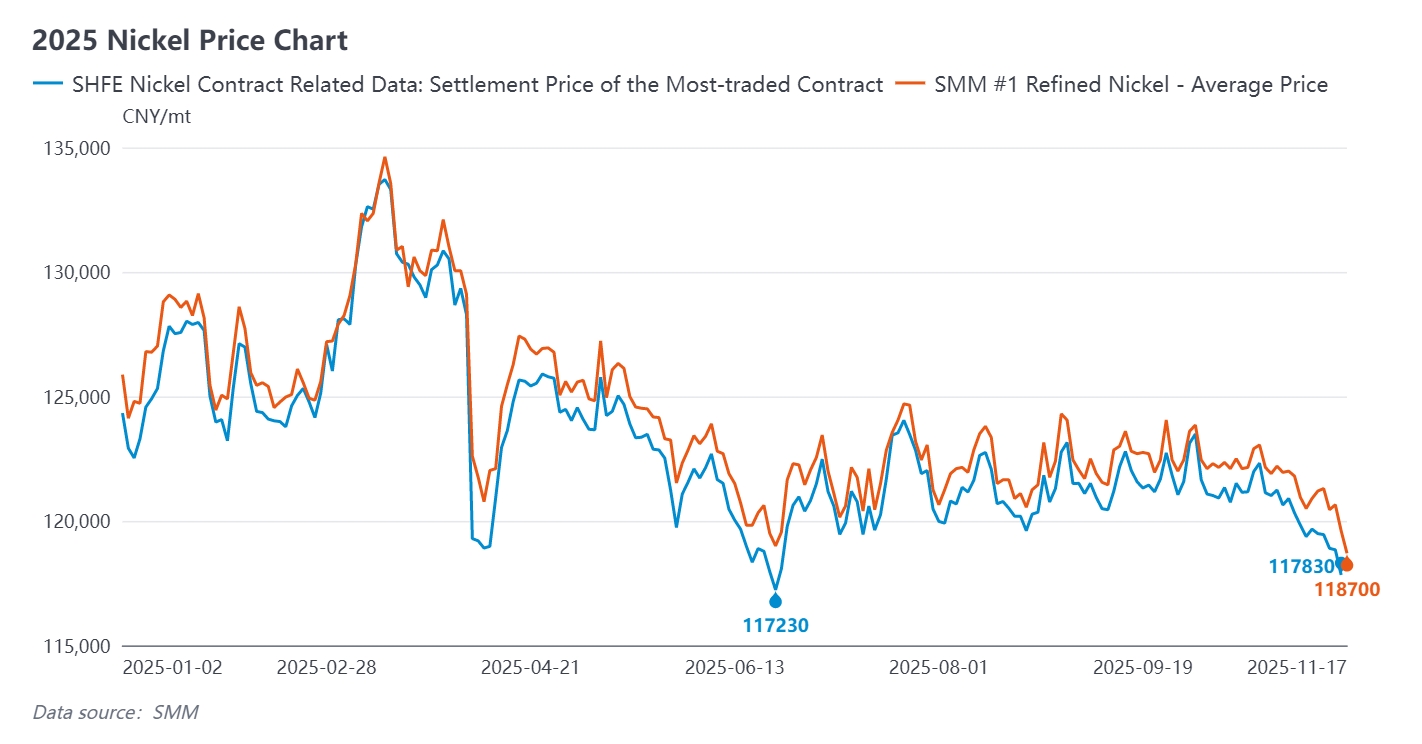

Since October 28, nickel prices have shifted from their previous volatile pattern into a unilateral downtrend, successively breaking through multiple key support levels, with market sentiment turning pessimistic. Specifically, the most-traded SHFE nickel contract fell from 121,000 yuan/mt to 116,730 yuan/mt on November 17, breaching the low seen in June. During the same period, LME nickel prices also dropped from $15,335/mt to below $14,800/mt, hitting a new low for the period. This round of decline marks nickel prices officially breaking below the 118,000–123,000 yuan/mt range that had persisted for nearly four months, with the technical chart showing a clear bearish alignment and the market's center further shifting downward.

Macro and Market Information

The global macro environment suppressed nickel prices in October-November 2025. China's CPI rose 0.2% YoY in October, while the manufacturing PMI production index fell to 49.7% and the new orders index dropped to 48.8%, both entering contraction territory, directly weakening demand expectations for downstream stainless steel and batteries. Although the market anticipated US Fed interest rate cuts, statements from US policymakers indicated that rate reductions would take time, delaying expectations of monetary policy easing. The US dollar index remained relatively strong, and as a cyclical commodity, nickel was subject to amplified macro fluctuations, lacking robust rebound momentum in its downward channel.

On November 10, Government Regulation No. 28/2025 (PP 28/2025) came into effect, with the Indonesian government restricting new investments in nickel smelters through "Industrial Business Permits" (IUI) to address global oversupply. Meanwhile, the Indonesian Ministry of Energy and Mineral Resources announced plans to reduce the 2026 nickel ore quota RKAB, which will be lower than the 319 million tons in 2025. However, this had limited short-term supply disruption, and market sentiment reacted minimally.

Fundamentals

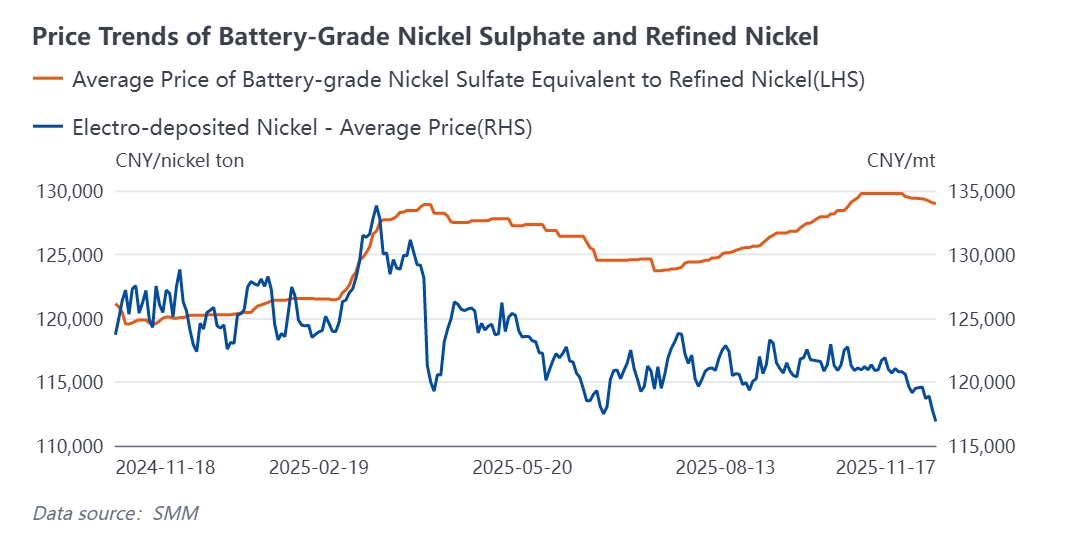

1. Due to the divergence between strong nickel sulphate prices and weak refined nickel prices, the average premium of SMM nickel sulphate over SMM electrodeposited nickel reached nearly 10,000 yuan in November. With a processing fee of 7,000 yuan, it is theoretically economical for refined nickel producers to switch to nickel sulphate production. Some enterprises showed a tendency to shift from refined nickel to nickel sulphate this month, potentially further driving expectations of a more relaxed nickel sulphate market. It is expected that the available volume of nickel sulphate for sale will rise, but the production schedule for ternary cathode material is expected to decline by year-end. In the context of weakening demand and increasing supply, there is downward pressure on nickel salt prices.

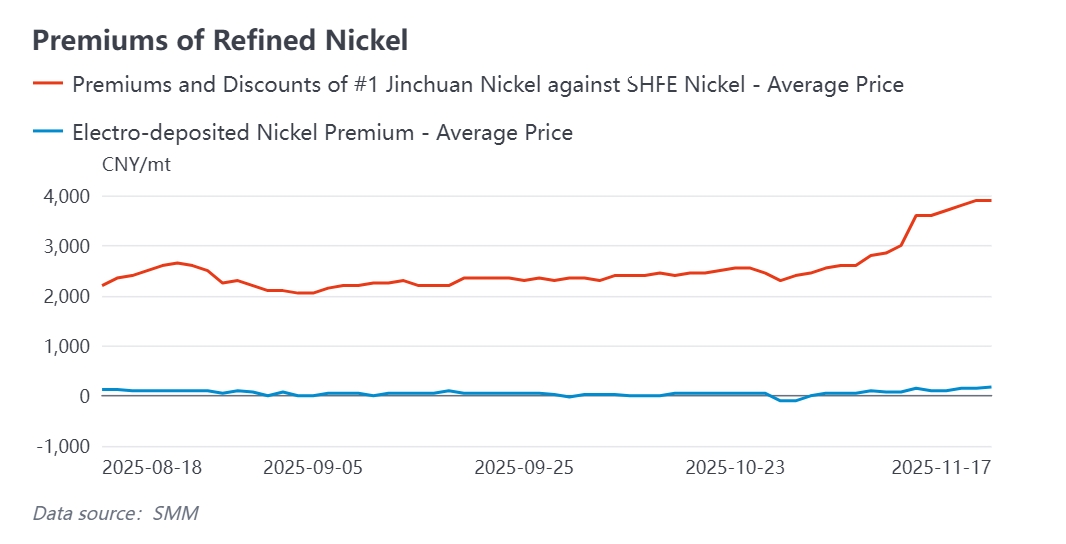

2. In terms of refined nickel supply and demand, due to some enterprises switching to nickel sulphate production, there are significant expectations for reduced refined nickel production in November. Producers and traders currently have a strong desire to hold prices firm, and the premium for refined nickel has strengthened notably since November. The premium for Jinchuan #1 refined nickel reached up to 4,000 yuan/mt, and the premium for mainstream domestic electrodeposited nickel also increased slightly. Alloy and special steel, as well as electroplating enterprises, shifted from an active purchasing attitude when nickel prices first fell to a wait-and-see approach after continuous price declines, waiting for a clear bottom before restocking as needed.

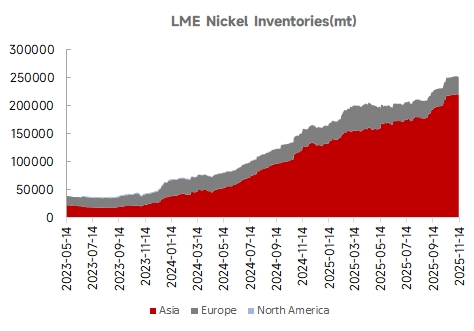

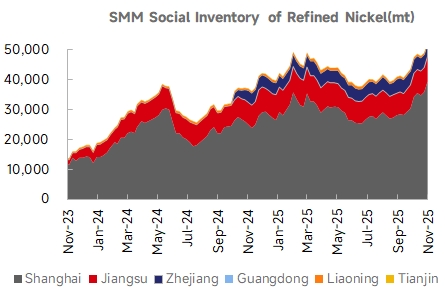

3. Inventory accumulation is the core pressure source for this downturn. As of November 17, LME nickel inventory reached 252,000 mt, and SMM refined nickel social inventory was as high as 53,000 mt, with global refined nickel inventory exceeding 300,000 mt, reaching a five-year high.

Outlook

After a continuous decline, nickel prices have shown signs of being oversold in the short term. With expectations of refined nickel production cuts, the recent pace of inventory accumulation is expected to slow down. Looking ahead, uncertainties in the Indonesian ore sector may provide a temporary rebound. However, under the dominance of the surplus logic, nickel prices are unlikely to achieve a genuine trend reversal and will continue to consolidate at the bottom. The price range for the most-traded SHFE nickel contract is expected to be 115,000-122,000 yuan/mt.